Global Recession Ahead?

Global Recession Ahead?

The one indicator that suggests the whole world may be on the brink...

From Dan Denning on the frozen plains of Laramie...

In today’s report, we travel forward in time by two weeks. On December 13th, you’re going to see a raft of headlines on the November Consumer Price Inflation (CPI) figures. This will happen on the first day of the last meeting of the year for the Federal Reserve’s Open Market Committee–the ‘Politburo’ of American finance that presumes to know the correct price of money.

If the inflation figures are ‘moderating,’ it will mean the Fed’s rate hike campaign is nearly over. Risk assets–stocks, corporate bonds, emerging market stocks–could rally to their hearts’ content into the Santa Season. And even bonds–having their worst year in American history since 1788–might show a little spunk.

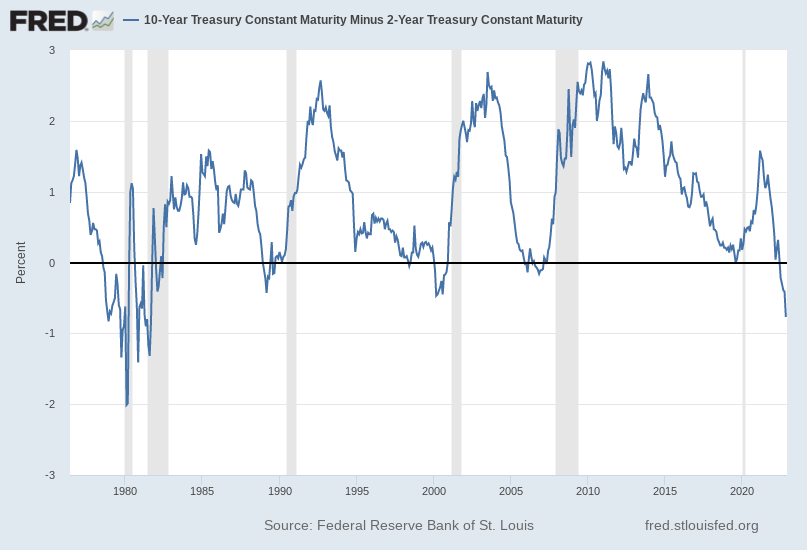

Blah blah blah. None of it matters. Take a look at the chart below. It’s crystal clear. When the yield curve inverts, the recession follows. In fact, most recent recessions in American history begin AFTER the Fed starts cutting rates. Even if inflation has peaked this year (this is Tom Dyson’s view, Bill and I aren’t so sure), the impact of a 2023 recession to corporate earnings and stock prices is not yet ‘priced in’ to the market.

Chairman Bill

By the way, before I continue, I should mention that Bill Bonner is safe and sound in Baltimore. We announced last week that he’s commissioned an ‘Annual Report to the Chairman’ to be prepared by the end of the year. In his capacity as founder and owner of the Agora Companies, Bill is privy to literally dozens of research reports, newsletters, trading systems, and more.

Earlier this year he decided to go back to his roots with Mark Hulbert over 40 years (The Hulbert Financial Digest) and evaluate what’s actually working in the stock market right now. That digest–designed to help individual investors rate and rank newsletters–was one of the first Bill published. The Chairmen’s Letter–which he hopes to publish for the first time later next month–will be his next. Stay tuned. Meanwhile, this from Deutsche Bank researchers:

“We see major stock markets plunging 25% from levels somewhat above today’s when the U.S. recession hits, but then recovering fully by year-end 2023, assuming the recession lasts only several quarters.’

The DB research note describes a 2023 recession as ‘temporarily painful.’ But that’s a matter of perspective, isn’t it? We recall Ronald Reagan’s line from the campaign trail in 1979: ‘A recession is when your neighbor loses his job. A Depression is when you lose your job. A recovery is when Jimmy Carter loses his job.’

It was a good line. But it was Reagan who had to deal with the ‘painful’ recession of 1982. Unemployment rose. As you can see on the chart above, the yield curve (10-year minus 2-year) inverted steeply before the recession. Then, the Fed began cutting rates. By 1982, both stocks and bonds had bottomed. And the stage was set for one of the greatest 40-year rallies in stock market history.

That’s what’s at stake in 2023. S&P Global Ratings analyst Ann Bovino says the ‘US economy appears to be teetering toward recession.’ She cites the Russia-Ukraine conflict, China’s lockdowns (more on that in second), and tensions over Taiwan. All valid. And what’s this?!

Recession Ahead?

Bloomberg reports the global yield curve is inverting. We didn’t even know that was a thing, to be honest, the ‘global’ yield curve. But it is. Specifically, it means the average yield on government bonds maturing in ten years is below the average yield on government bonds maturing in one to three years (as measured by the Bloomberg Aggregate Bond Index). That kind of inversion–which hasn’t happened this millennium–would also signal a recession (of the global kind).

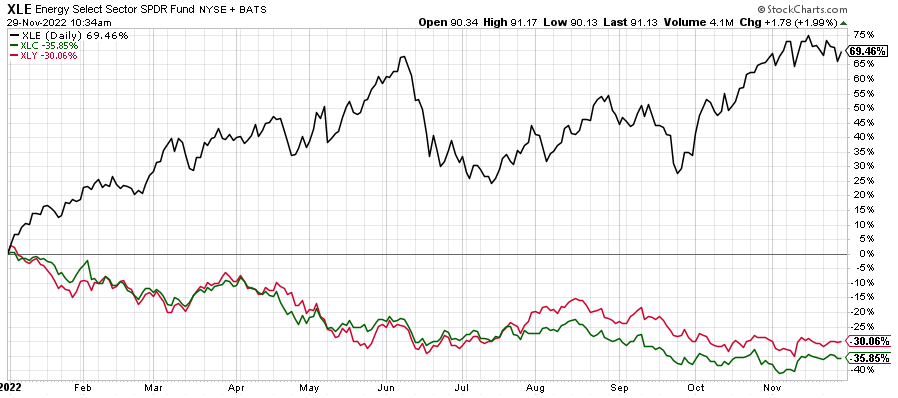

Is there any place to hide in a market like that? Only three of the twelve S&P sectors are positive, year-to-date. XLU (Utilities) and XLP (Consumer Staples) are barely in positive territory. Energy stocks are up 69%, as you can see on the chart below. XLC (Communication Services) and XLY (Consumer Discretionary) are the dogs of the sector funds.

But wait! Oil is under $80 per barrel. And wouldn’t a global recession be negative for energy demand? And if XLE was the best performing sector in 2022, what are the odds it would repeat in 2023?

All valid questions, the answers to which are beyond the scope of a free daily email. But we’re keeping a close eye on things for our Trade of the Decade. Most of the biggest oil and gas producers are trading at a forward P/E under ten and a Price/Sales ratio under two. Tech, by comparison, is still expensive.

Also keep in mind that total global oil demand was 99.7 million barrels per day (mbpd) in 2019. The authoritarian response to the pandemic was to shut down the entire global economy and lock everyone inside for months. Even then, global oil demand only fell to 91 mbpd in 2019. It’s on pace to equal the 2019 level this year–with a cold hard winter setting in over Europe and North America.

Until next time,

Dan

PS About China. No one really knows what’s happening there right now. Is it another Tiananmen Square? Will Xi crack down on millions of people protesting his ‘Zero Covid’ policies? Will China face a major public health crisis?

Who knows? What we DO know is that Apple restricted the use of its AirDrop feature in iPhones in a software update that went out last week. The AirDrop feature allows direct communication between iPhones without going through a cell network (which can be monitored or shut down by the authorities). Chinese protesters have reportedly been using AirDrop to communicate and organize and evade.

Why does Silicon Valley hate free speech so much? Leave a comment below if you know the answer.

In the meantime, Apple is the last of the Big Tech ‘Generals’ standing. It hasn’t taken out its June low of $130/per share. All the other Big Tech Generals did. The company may face interrupted production of its iPhones at the FoxConn factory in China, where its iPhone Pro is produced. Wouldn’t that be something if it’s China that causes Apple to finally crack?

Why does Big Tech hate free speech so much? The answer is simple and obvious: anyone, any group, any government which hates free speech does so, because they don't think their audience/constituency can be trusted to make the "right" choice, i.e. the GROUP's choice, and the audience/constituency must therefore be corralled, impinged, restricted, or otherwise controlled in order to insure the proper "choice' by the audience/constituency. That sad fact is depressing enough; worse still is the fact that they get away with it. Best always. PM

without the technology companies there can be no elitist narrative echo chamber. Propagated and propagandized by our friendly democratic party and deep state operatives in the intelligence and justice departments. Hence the apoplectic response to Musk opening Twitter up to non-narrative voices: such a crime!!! I applaud his efforts to open the platform to free speech -regardless of narrative support. I wish the other technocrats had the balls to stand up to these true "fascists"